Login

Just a moment...

Press 'Enter' to add multiple search terms. Rules for Better Search

Press 'Enter' after typing page number.

Press 'Enter' after typing page number.

No Folders have been created

Are you sure you want to delete "My most important" ?

NOTE:

Press 'Enter' after typing page number.

Press 'Enter' after typing page number.

All News

Press 'Enter' after typing page number.

Press 'Enter' after typing page number.

All News

Note

Bookmark

Share

Don't have an account? Register Here

Monetary Policy Decisions

The Monetary Policy Committee (MPC) held its 55th meeting from June 4 to 6, 2025 under the chairmanship of Shri Sanjay Malhotra, Governor, Reserve Bank of India. The MPC members Dr. Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr. Poonam Gupta and Dr. Rajiv Ranjan attended the meeting.

2. After assessing the current and evolving macroeconomic situation, the MPC voted to reduce the policy repo rate by 50 basis points (bps) to 5.50 per cent with immediate effect. Consequently, the standing deposit facility (SDF) rate under the liquidity adjustment facility (LAF) shall stand adjusted to 5.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate to 5.75 per cent. This decision is in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

Growth and Inflation Outlook

3. The uncertainty around the global economic outlook has ebbed somewhat since the MPC met in April in the wake of temporary tariff reprieve and optimism around trade negotiations. However, it continues to remain elevated to weaken sentiments and lower global growth prospects. Accordingly, global growth and trade projections have been revised downwards by multilateral agencies. Market volatility has eased in the recent period with equity markets staging a recovery, dollar index and crude oil softening though gold prices remain high.

4. According to the provisional estimates released by the National Statistical Office (NSO) on May 30, 2025, real GDP growth in Q4:2024-25 stood at 7.4 per cent as against 6.4 per cent in Q3. On the supply side, real gross value added (GVA) rose by 6.8 per cent in Q4:2024-25. For 2024-25, real GDP growth was placed at 6.5 per cent, while real GVA recorded a growth of 6.4 per cent.

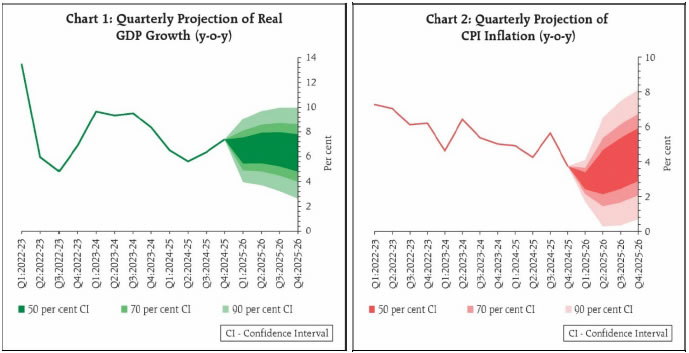

5. Going forward, economic activity continues to maintain the momentum in 2025-26, supported by private consumption and traction in fixed capital formation. The sustained rural economic activity bodes well for rural demand, while continued expansion in services sector is expected to support the revival in urban demand. Investment activity is expected to improve in light of higher capacity utilization, improving balance sheets of financial and non-financial corporates, and government’s capital expenditure push. Trade policy uncertainty continues to weigh on merchandise exports prospects, while the conclusion of free trade agreement (FTA) with the United Kingdom and progress with other countries is supportive of trade activity. On the supply side, agriculture prospects remain bright on the back of an above normal south-west monsoon forecast and resilient allied activities. Services sector is expected to maintain its momentum. However, spillovers emanating from protracted geopolitical tensions, and global trade and weather-related uncertainties pose downside risks to growth. Taking all these factors into account, real GDP growth for 2025-26 is projected at 6.5 per cent, with Q1 at 6.5 per cent, Q2 at 6.7 per cent, Q3 at 6.6 per cent, and Q4 at 6.3 per cent (Chart 1). The risks are evenly balanced.

6. CPI headline inflation continued its declining trajectory in March and April, with headline CPI inflation moderating to a nearly six-year low of 3.2 per cent (year-on-year) in April 2025. This was led mainly by food inflation which recorded the sixth consecutive monthly decline. Fuel group witnessed a reversal of deflationary conditions and recorded positive inflation prints during March and April, partly reflecting the hike in LPG prices. Core inflation remained largely steady and contained during March-April, despite increase in gold prices exerting upward pressure.

7. The outlook for inflation points towards benign prices across major constituents. The record wheat production and higher production of key pulses in the Rabi crop season should ensure adequate supply of key food items. Going forward, the likely above normal monsoon along with its early onset augurs well for Kharif crop prospects. Reflecting this, inflation expectations are showing a moderating trend, more so for the rural households. Most projections point towards continued moderation in the prices of key commodities, including crude oil. Notwithstanding these favourable prognoses, we need to remain watchful of weather-related uncertainties and still evolving tariff related concerns with their attendant impact on global commodity prices. Taking all these factors into consideration, and assuming a normal monsoon, CPI inflation for the financial year 2025-26 is now projected at 3.7 per cent, with Q1 at 2.9 per cent; Q2 at 3.4 per cent; Q3 at 3.9 per cent; and Q4 at 4.4 per cent (Chart 2). The risks are evenly balanced.

Rationale for Monetary Policy Decisions

8. Inflation has softened significantly over the last six months from above the tolerance band in October 2024 to well below the target with signs of a broad-based moderation. The near-term and medium-term outlook now gives us the confidence of not only a durable alignment of headline inflation with the target of 4 per cent, as exuded in the last meeting but also the belief that during the year, it is likely to undershoot the target at the margin. While food inflation outlook remains soft, core inflation is expected to remain benign with easing of international commodity prices in line with the anticipated global growth slowdown. The inflation outlook for the year is being revised downwards from the earlier forecast of 4.0 per cent to 3.7 per cent. Growth, on the other hand, remains lower than our aspirations amidst challenging global environment and heightened uncertainty.

9. Thus, it is imperative to continue to stimulate domestic private consumption and investment through policy levers to step up the growth momentum. This changed growth-inflation dynamics calls for not only continuing with the policy easing but also frontloading the rate cuts to support growth. Accordingly, the MPC voted to reduce the policy repo rate by 50 bps to 5.50 per cent. Dr. Nagesh Kumar, Prof. Ram Singh, Dr. Rajiv Ranjan, Dr. Poonam Gupta and Shri Sanjay Malhotra, voted to decrease the policy repo rate by 50 bps. Shri Saugata Bhattacharya voted for a 25 bps cut in repo rate.

10. After having reduced the policy repo rate by 100 bps in quick succession since February 2025, under the current circumstances, monetary policy is left with very limited space to support growth. Hence, the MPC also decided to change the stance from accommodative to neutral. From here onwards, the MPC will be carefully assessing the incoming data and the evolving outlook to chart out the future course of monetary policy in order to strike the right growth-inflation balance. The fast-changing global economic situation too necessitates continuous monitoring and assessment of the evolving macroeconomic outlook.

11. The minutes of the MPC’s meeting will be published on June 20, 2025.

12. The next meeting of the MPC is scheduled from August 4 to 6, 2025.

(Puneet Pancholy)

Chief General Manager

Press 'Enter' after typing page number.