Login

Generate professional replies, appeals, opinions to Show Cause Notices, assessment orders, audit objections, and other legal communications using TaxTMI's AI Drafter.

Generate professional replies, appeals, opinions to Show Cause Notices, assessment orders, audit objections, and other legal communications using TaxTMI's AI Drafter.

Just a moment...

Generate professional replies, appeals, opinions to Show Cause Notices, assessment orders, audit objections, and other legal communications using TaxTMI's AI Drafter.

Press 'Enter' to add multiple search terms. Rules for Better Search

Press 'Enter' after typing page number.

Press 'Enter' after typing page number.

No Folders have been created

Are you sure you want to delete "My most important" ?

NOTE:

Press 'Enter' after typing page number.

Press 'Enter' after typing page number.

All News

Press 'Enter' after typing page number.

Press 'Enter' after typing page number.

All News

Note

Bookmark

Share

Don't have an account? Register Here

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (August 8, 2024) decided to:

Consequently, the standing deposit facility (SDF) rate remains unchanged at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

Assessment and Outlook

2. The global economic outlook remains resilient although with some moderation in pace. Inflation is retreating in major economies but services price inflation persists. International prices of food, energy and base metals have eased since the last policy meeting. With varying growth-inflation prospects, central banks are diverging in their policy paths. This is creating volatility in financial markets. Amidst recent global sell offs in equities, the dollar index has weakened, sovereign bond yields have eased sharply and gold prices have soared to record highs.

3. Domestic economic activity continues to sustain its momentum. After a weak and delayed start, the cumulative southwest monsoon rainfall has picked up with improving spatial spread. By August 7, 2024, it was 7 per cent above the long period average. This has supported kharif sowing, with total area sown as on August 2, being 2.9 per cent higher than a year ago. Industrial output registered an expansion of 5.9 per cent (y-o-y) in May 2024. Core industries rose by 4.0 per cent in June, against 6.4 per cent in May. Other high frequency indicators released during June-July 2024 indicate expansion of services sector activity, ongoing revival of private consumption, and signs of pickup in private investment activity. Merchandise exports, non-oil non-gold imports, services exports and imports expanded during April-June.

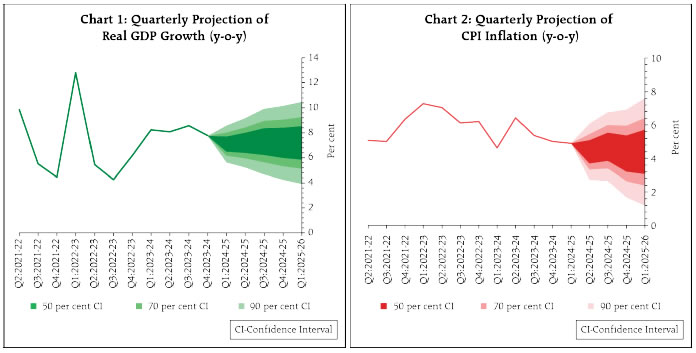

4. Going forward, the Indian Meteorological Department’s (IMD) projection of above normal southwest monsoon and healthy kharif sowing will support improving rural demand. The sustained momentum in manufacturing and services suggests steady urban demand. High frequency indicators of investment activity as evident in strong expansion in steel consumption, high capacity utilisation, healthy balance sheets of banks and corporates, and the Government’s continued thrust on infrastructure spending, point to a robust outlook. Improving world trade prospects could support external demand. Headwinds from geopolitical tensions, volatility in international commodity prices and geoeconomic fragmentation, however, pose risks to the outlook. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.2 per cent with Q1 at 7.1 per cent; Q2 at 7.2 per cent; Q3 at 7.3 per cent; and Q4 at 7.2 per cent. Real GDP growth for Q1:2025-26 is projected at 7.2 per cent (Chart 1). The risks are evenly balanced.

5. Headline inflation increased to 5.1 per cent in June 2024 after remaining steady at 4.8 per cent during April-May 2024. Worsening of food inflation pressures – driven primarily by a sharp increase in prices of vegetables, pulses and edible oils along with a pick-up in inflation across cereals, milk, fruits and prepared meals – pushed up headline inflation. The fuel group remained in deflation, reflecting the cumulative impact of the sharp cuts in LPG price in August 2023 and March 2024. Core (CPI excluding food and fuel) inflation at 3.1 per cent in May-June touched a new low in the current CPI series, with core services inflation also at its lowest in the series.

6. Headline inflation has moderated from its peak but unevenly. Looking ahead, food price momentum has remained elevated in July. In Q2:2024-25, though favourable base effects are large, the sharper uptick in price momentum relative to earlier expectations is likely to result in a shallower softening of CPI headline inflation. Inflation is expected to edge up in Q3 as favourable base effects taper off. The steady progress in monsoon, pick-up in kharif sowing, adequate buffer stocks of foodgrains and easing global food prices are positives for containing food price pressures. Adverse climate events remain an upside risk to food inflation. Crude oil prices continue to be volatile on demand concerns and geopolitical tensions. The revision in mobile tariff rates is likely to lead to an increase in core inflation. Manufacturing, services and infrastructure firms surveyed by the Reserve Bank expect a pickup in selling prices in the second half of this year. Households’ inflation expectations have also gone up and consumer confidence has weakened. Assuming a normal monsoon, CPI inflation for 2024-25 is projected at 4.5 per cent with Q2 at 4.4 per cent; Q3 at 4.7 per cent; and Q4 at 4.3 per cent. CPI inflation for Q1:2025-26 is projected at 4.4 per cent (Chart 2). The risks are evenly balanced.

7. The MPC expects domestic growth to hold up on the strength of investment demand, steady urban consumption and rising rural consumption. Risks from volatile and elevated food prices remain high, which may adversely impact inflation expectations and result in spillovers to core inflation. There are also indications of core inflation bottoming out. Accordingly, the MPC decided to remain watchful on how these forces play out, going forward. The MPC stays resolute in its commitment to aligning inflation to the 4 per cent target on a durable basis. In these circumstances, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent in this meeting. The MPC reiterates the need to continue with the disinflationary stance, until a durable alignment of the headline CPI inflation with the target is achieved. Enduring price stability sets strong foundations for a sustained period of high growth. Hence the MPC also considers it appropriate to continue with the disinflationary stance of withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

8. Dr. Shashanka Bhide, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to keep the policy repo rate unchanged at 6.50 per cent. Dr. Ashima Goyal and Prof. Jayanth R. Varma voted to reduce the policy repo rate by 25 basis points.

9. Dr. Shashanka Bhide, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth. Dr. Ashima Goyal and Prof. Jayanth R. Varma voted for a change in stance to neutral.

10. The minutes of the MPC’s meeting will be published on August 22, 2024.

11. The next meeting of the MPC is scheduled during October 7 to 9, 2024.

(Puneet Pancholy)

Chief General Manager

Press 'Enter' after typing page number.