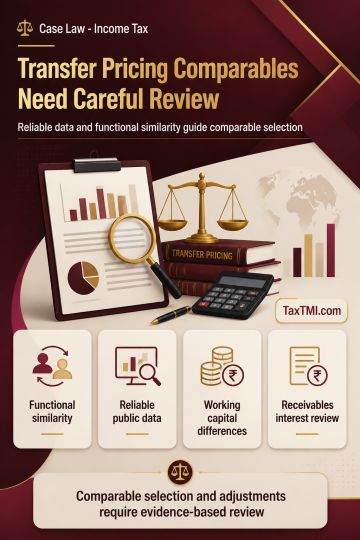

Transfer pricing comparability requires functional alignment, reliable financial data, and careful review of working capital and receivables adjustmen...

Transfer pricing rules require benchmarking corporate guarantees and associated-enterprise advances, while invalid domestic-transaction adjustments ca...

CESTAT NEW DELHI addressed unjust enrichment in a refund claim. The appellant sought a refund of Rs. 1,23,70,024 u/s the Tribunal's order. The appellant failed to prove it wouldn't unjustly enrich itself if refunded. The Credit Note indicated the amount was to be paid to specific entities upon refund. No evidence showed these entities didn't collect service tax from flat allottees. The Assistant Commissioner rightly decided the refund should go to the Consumer Welfare Fund. The Tribunal's final order required proof of no unjust enrichment for refund eligibility. The Commissioner (Appeals) decision was upheld, dismissing the appeal. The appellant couldn't contest the unjust enrichment principle after the Tribunal's final order.

CESTAT NEW DELHI addressed unjust enrichment in a refund claim. The appellant sought a refund of Rs. 1,23,70,024 u/s the Tribunal's order. The appellant failed to prove it wouldn't unjustly enrich itself if refunded. The Credit Note indicated the amount was to be paid to specific entities upon refund. No evidence showed these entities didn't collect service tax from flat allottees. The Assistant Commissioner rightly decided the refund should go to the Consumer Welfare Fund. The Tribunal's final order required proof of no unjust enrichment for refund eligibility. The Commissioner (Appeals) decision was upheld, dismissing the appeal. The appellant couldn't contest the unjust enrichment principle after the Tribunal's final order.

Note: It is a system-generated summary and is for quick reference only.