Terminal gate verification for transshipment containers shifts to operators, while Customs controls and discrepancy reporting requirements remain mand...

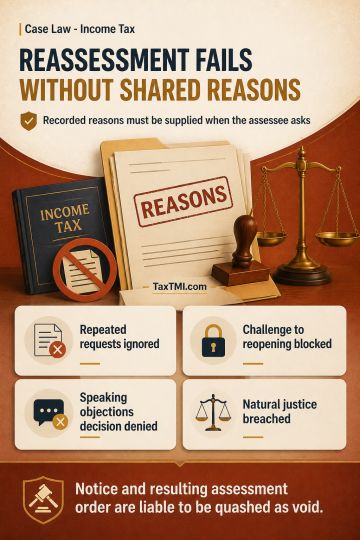

Disallowance of deduction on account of payment to L&T Ltd. for reimbursement of employee related option scheme was rejected as the payments were not doubted by the AO/CIT(A), TDS was deducted, and no contrary evidence was provided. The expenditure incurred on a cost-to-cost basis for deputed employees was held allowable u/s 37(1). Regarding software license fees, the ITAT held that short-term licenses facilitating business operations qualify as revenue expenditure as no new asset was created. Deduction u/s 10A for the STP unit's first year was allowed as the assessee exported computer software in convertible foreign exchange per CBDT Circular 2/2013 and the Karnataka HC ruling. Loss on forward contracts was treated as a regular business loss u/s 43(5) as the assessee was not a forex dealer but an exporter hedging against losses through forward contracts related to export services.

Disallowance of deduction on account of payment to L&T Ltd. for reimbursement of employee related option scheme was rejected as the payments were not doubted by the AO/CIT(A), TDS was deducted, and no contrary evidence was provided. The expenditure incurred on a cost-to-cost basis for deputed employees was held allowable u/s 37(1). Regarding software license fees, the ITAT held that short-term licenses facilitating business operations qualify as revenue expenditure as no new asset was created. Deduction u/s 10A for the STP unit's first year was allowed as the assessee exported computer software in convertible foreign exchange per CBDT Circular 2/2013 and the Karnataka HC ruling. Loss on forward contracts was treated as a regular business loss u/s 43(5) as the assessee was not a forex dealer but an exporter hedging against losses through forward contracts related to export services.

Note: It is a system-generated summary and is for quick reference only.